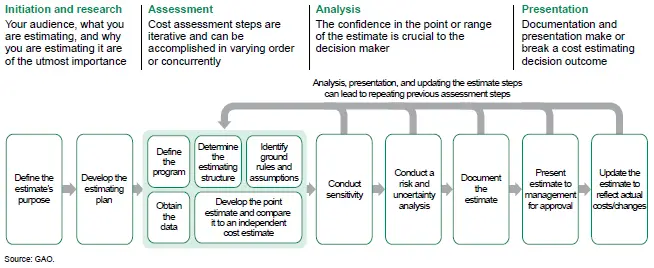

The Government Accountability Office (GAO) Cost Estimating Process consists of twelve (12) steps. Each step builds upon each other to develop and comprehensive and complete cost estimate. Each of the 12 steps is important for ensuring that high-quality cost estimates are developed and delivered in time to support important decisions.

Steps: Tasks Breakdown of the GAO 12 Steps

Guide: GAO Cost Estimating and Assessment Guide

12 Step GAO Cost Estimating Process:

- Step 1: Define Estimate’s Purpose

- Step 2: Develop Estimating Plan

- Step 3: Define Program Characteristics

- Step 4: Determine Estimating Structure

- Step 5: Identify Ground Rules and Assumptions

- Step 6: Obtain Data

- Step 7: Develop Point Estimate and Compare it to an Independent Cost Estimate

- Step 8: Conduct Sensitivity Analysis

- Step 9: Conduct Risk and Uncertainty Analysis

- Step 10: Document the Estimate

- Step 11: Present Estimate to Management for Approval

- Step 12: Update the Estimate to Reflect Actual Costs and Changes

Certain best practices should be followed if accurate and credible cost estimates are to be developed. These best practices represent an overall process of established, repeatable methods that result in high-quality cost estimates that are comprehensive and accurate and that can be easily and clearly traced, replicated, and updated.

AcqLinks and References:

Updated: 7/24/2021

Rank: G7