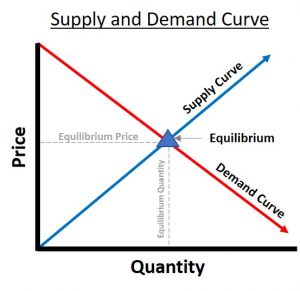

Supply and Demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good will vary until it settles at a point where the quantity demanded by consumers will equal the quantity supplied by producers resulting in an economic equilibrium of price and quantity. This relationship between supply and demand can be seen in a plot of the classic supply-demand curve on the right. In its simplest terms; When prices go up, supply goes up and demand goes down. When prices go down, demand goes up and supply goes down. [1]

Definition: The law of supply and demand is a theory that explains the interaction between the sellers of a resource and the buyers for that resource.

What are the Supply and Demand Laws?

The Supply and Demand model has two “laws,”: the (1) Law of Demand and the (2) Law of Supply. These laws interact with each other to determine the market price and volume of goods.

(1) What is the Law of Demand?

The Law of Demand refers to the number of products people are willing to buy at different prices at a specific time. The law states that the higher the product price, the fewer people will demand the product. As a consumer, the higher a product costs, the less the amount of the product the consumer will purchase. This means the opportunity cost of buying that product goes down. [2]

Factors that influence the supply are:

- Consumer Preference

- Influence

- Number of Sellers

- Taxes and Regulations

(2) What is the Law of Supply?

Supply refers to the quantities of products manufacturers or owners are willing to sell at different prices at a specific time. The higher the price will result in the higher quantity supplied. As a seller, the opportunity cost of each product is higher, so they want to sell more, and producers want to produce more. [1]

Factors that influence the supply are:

- Labor and Materials costs

- Technology availability

- Number of sellers

- Capacity

- Taxes and Regulations

Supply and Demand Outcomes

The four (4) basic outcomes of supply and demand are: [3]

- If demand increases and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price.

- If demand decreases and supply remains unchanged, a surplus occurs, leading to a lower equilibrium price.

- If demand remains unchanged and supply increases, a surplus occurs, leading to a lower equilibrium price.

- If demand remains unchanged and supply decreases, a shortage occurs, leading to a higher equilibrium price.

What is Supply and Demand Equilibrium?

The market price is the intersection of the demand price and quantities of products manufactured, and the intersection is called the equilibrium price or Market Clearing Price. The equilibrium price is the price at which the producer can sell all the units he wants to produce, and the buyer can buy all the units he wants.

It is visualized on a chart at the intersection of the supply and demand curve. This intersection is the market price at which suppliers bring to market that same quantity of product that consumers will be willing to buy. They then say that Supply and Demand are in equilibrium. [1]

Purpose of the Supply and Demand Theory

The purpose of the Supply and Demand theory is to help people, businesses, bankers, investors, entrepreneurs, economists, government, and others understand and predict conditions in the market for best optimization.

Factors that Affect Supply and Demand

Factors that affect supply: In industries where suppliers don’t want to lose money when product prices are lower than production costs, supply tends to go down toward zero. Price elasticity will also depend on the number of sellers, their total production capacity, how easily it can be lowered or raised, and how competitive the industry is. Taxes and regulations may matter as well.

Factors that affect demand: are how many people want to buy something. Some of the most important things that affect demand are consumer income, preferences, and willingness to switch from one product to another. Consumer preferences will depend, in part, on a product’s market penetration, since the marginal utility of goods diminishes as the quantity owned increases. The first house changes your life more than the fifth one you buy, and the table in your living room is more useful than the one in your garage.

What Is an Example of the Law of Supply and Demand?

A bread company wants to introduce a new french bread to its market at the best possible price. To ensure the lowest production price, the manufacturer gets bids from many suppliers to obtain the lowest possible price for manufacturing the new bread. The lower the cost of the bread, the more profit the company can make if it determines the best price that sells the most quantity of bread. The equilibrium (Market Price) between the quantity of bread sold and the price should bring the most profit.

AcqLinks and References:

- [1] Nickels and McHugh, “Understanding Business” McGraw-Hill Irwin 2010

- Price Theory – Supply and Demand Lecture

Updated: 3/8/2023

Rank: G12.8